This article is being co-hosted on Maple Leafs Hot Stove as well as on my own site, OriginalSixAnalytics.com. Find me @OrgSixAnalytics on twitter.

Author’s note: For those who noticed, my apologies for the four-plus month gap between articles in this ‘Mythbusters’ series. This piece has been about 80% complete since September, but between my day job and hockey consulting work, I have had limited time to write. While Stamkos’ contract negotiation is now very old news, the analysis herein remained meaningful, so I figured I would finish this up and publish regardless.

As introduced in my article in September on the topic of the Maple Leafs’ use of analytics, this piece will be the second of my ‘Mythbusters’ series. The point of this series was to write a short set of articles that use data and objective analysis to try to go against the grain on some of the narratives that came out over the summer of 2016.

In this article, my topic will be the (now ice-cold) Steven Stamkos free agency situation. Although I am posting this on Maple Leafs Hot Stove, this ‘myth’ is one that has been spread around the league at large. Rumours of Buffalo or Detroit offering Stamkos an AAV of $10-11M+ had people suggesting Steven left an annual $2M-3M+ ‘on the table’ to stay with Tampa. Stamkos was sometimes quoted as having “taken a big pay cut for the chance at a cup”.

Today, I will argue that – although those teams or Toronto may have given Stamkos ‘headline’ contract offers that are significantly above the $8.5M AAV he ultimately took in Tampa Bay – Steven actually maximized his own income by staying in Tampa. The most important factor here will be estimating the tax impact of Stamkos’ hypothetical contract offers, which we will get into shortly.

Most people give Steven credit for his commitment to winning by re-signing with a team that has been to two consecutive Conference Finals, for embracing his role as a franchise player and team captain in Tampa, and for staying loyal to his teammates. But not many have acknowledged that he’s actually making about as much money as possible by staying in Florida as well.

Putting aside Stamkos’ current injury and reflecting back to his time of signing, let’s dig in. Through the lens of the Stamkos situation, we can better understand tax considerations for NHL players and professional athletes more widely.

Situation Recap

Last spring, I wrote two articles about Steven Stamkos: one estimated Stamkos’ market value, and the second was a long-term analysis of the Leafs’ salary cap – to see if they had room for him in their ‘plan’. In these, I argued Stamkos’ was ‘worth’ anywhere from $9.5M to $10.5M of AAV for the maximum possible term, and that the Leafs should attempt to sign him for the $9.5M-$10M range.

As we all know, Stamkos ‘shocked’ everyone by re-signing with Tampa Bay days before reaching free agency (granted, he had had the chance to speak to other teams) at a contract value that had previously been released publicly: $8.5M over eight years. But did he “leave money on the table”?

Adjusting Stamkos’ Contract for Tax Implications

It is easy to discount the impact of taxes – especially when it isn’t your money. Unfortunately, the fact of the matter is that no employed person in North American walks home with their ‘full’ salary in hand – the tax-man has to take his slice first. Depending on the region, someone who ‘makes’ $50K per year may take home $40K, and someone who makes $150K will keep maybe $115K – and the highest brackets are even more impactful when these numbers become millions.

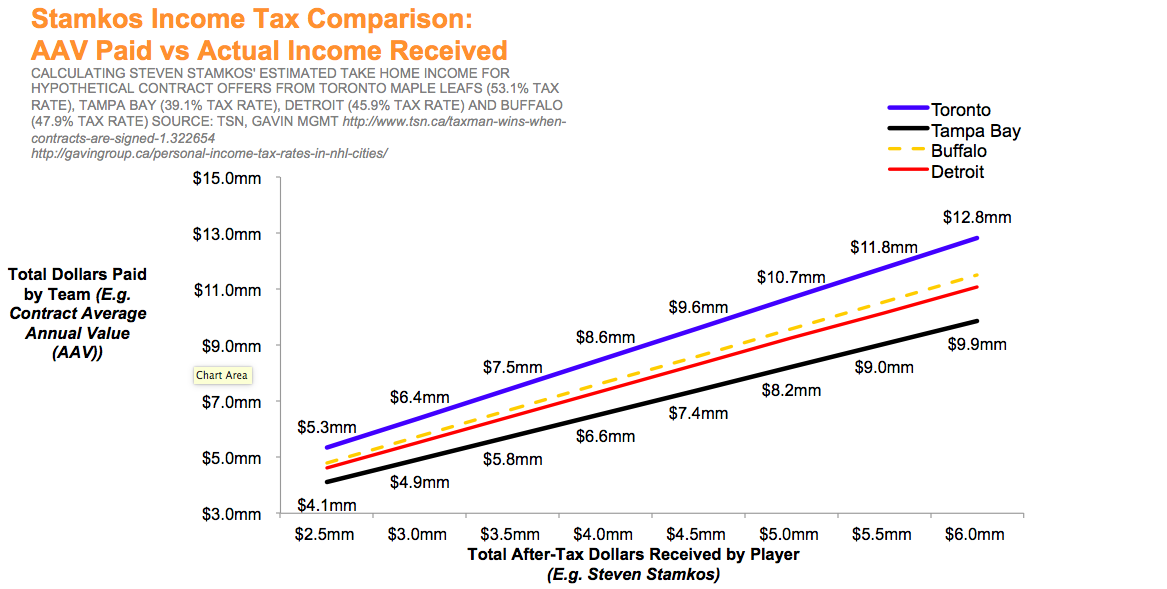

Looking at fully-burdened income tax rates (including both federal and state/provincial), Ontario and Florida are at opposite ends of the spectrum — Ontario’s top tax bracket being ~53% and Florida’s being ~39%. In order to illustrate this impact, the chart below shows what each team has to pay (on the y-axis) in order for Stamkos to receive a given amount of take-home pay (on the x-axis).

This is bit of a simplified approach, so to clarify some of my assumptions:

- Only applies the highest tax bracket (rather than each marginal bracket), which usually takes effect after a couple hundred thousand in income

- Combines all levels of taxes (federal, state/provincial)

- Excludes minor taxes/fees associated with playing away games in different cities/states

- Ignores the impact of escrow, which would hit all teams equally as a percentage

What does this chart tell us? Quite simply, for Steven (or any player) to take home the exact same amount of money, Tampa Bay can pay him considerably less than other teams on an AAV basis, and still be ‘matching’ or exceeding the offers on an ‘actual take-home pay’ basis. This amounts to a substantial financial competitive advantage for Tampa Bay (or the Florida Panthers), and a distinct disadvantage for high tax region teams like Toronto.

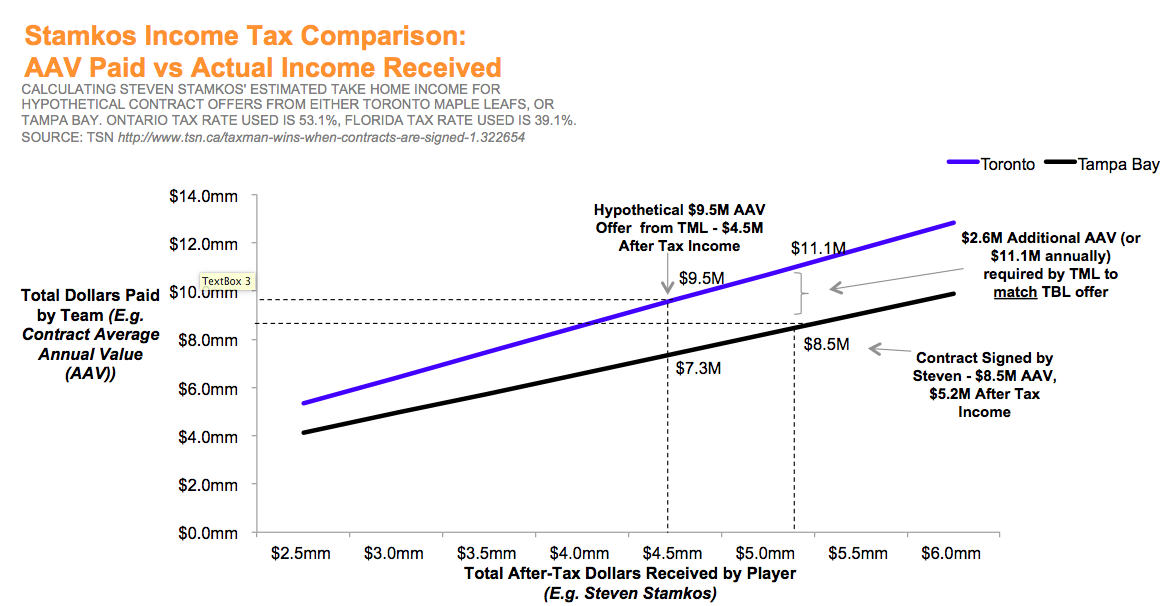

Now, given the public storyline was that Stamkos’ top two choices were Tampa or Toronto, let’s see how this would have made hypothetical offers to Stamkos from Toronto and Tampa Bay look on an ‘actual take-home’ pay basis.

As we can see, if TML had offered my proposed $9.5M to Stamkos, Steven would only get to keep ~$4.5M per year. At the $8.5M offer that he ultimately accepted from Tampa, the much superior tax rate allows Stamkos to take home pay of $5.2M, a gap of $700K per season.

For Toronto to have matched Tampa’s $8.5M AAV offer, it would have cost them $11.1M AAV per year on Stamkos, which was undoubtedly outside of the range that Lamoriello, Pridham & Co were willing to accept. Put differently – in order for Tampa to match a hypothetical $9.5M AAV offer from Toronto, they would have only needed to give Stamkos $7.3M.

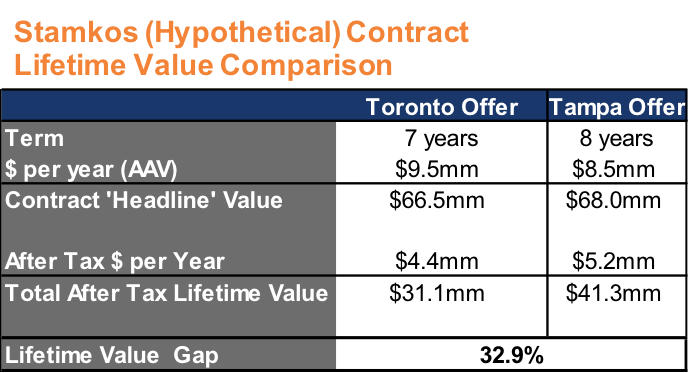

The table below summarizes how this tallies up over the life of his contract, including the fact that Tampa can give him one more year than any other team:

Thanks to TSN’s helpful after-tax take home pay calculator, we can see that even if Buffalo or Detroit offered Stamkos $11.0M AAV, they only come out at $40.2M and $41.7M in after-tax total contract value respectively — essentially matching the existing offer that Tampa Bay had already made.

Conclusion

Financially speaking, it should now be clear that Steven did not ‘leave money on the table’ to stay in Tampa. In fact, he made just about the maximum possible amount when compared to rumoured offers from other teams. Further, I haven’t spent any time in this article looking at the wide range of other factors that could have caused Stamkos to want to re-sign in Tampa, including:

- Stanley Cup Competitiveness (near term & medium term)

- Steven’s Role & Contribution (as Captain)

- Total Financial Compensation

- ‘Legacy’ Potential

- Geography (proximity to friends and family)

Tampa certainly outperforms Toronto on (a), and (b), above, and we just showed he was actually maximizing his total after-tax compensation (c) by staying in Tampa as well. Sure, Toronto would be close to friends and family and could have created an unbelievable ‘legacy’ (should he have helped the team become a contender), but it is hard to knock a superstar athlete for prioritizing the team he captains, who is a regular Cup-contender, and who has also given him the best financial offer. It should be no wonder to us as outsiders that Steve Yzerman succeeded again in a long-drawn-out negotiation where his offer was fair – and final.